Chapter 1 Music Economy

The music.dataobservatory.eu monitors the music markets with an economic methodology: we not only measure market volumes and prices, but we also measure both demand- and supply side indicators so that we can forecast future market volumes or prices. (See 4 Innovation pillar — 4.2 Forecasting)

Music is not a purely market activity. Music and music services have consumers who pay for it one way or another, but there are non-market forms of music (for example, in liturgy) and music markets are overshadowed by a very large illegal market. Therefore, instead of “music consumption” we use the more appropriate statistical terms of access and participation.

1.1 Music Industry

The three income streams model is essentially a value chain based model that was developed in the United States (Hull et al. 2011) and adopted by the European Commission’s Joint Research Center for European CCI policy purposes (Leurdijk and Ottilie 2012). We made minor adaptations to the three-income model for applicability in less developed markets in Central and Eastern Europe.

While in the original American model sound recordings are the “main” income stream, currently, especially in Central Europe, the live performance stream earns the most income for a typical musician. The author’s stream is the oldest part–traditionally and analytically–of the music industry, includeing revenue streams based on musical works exploited by music publishers and via author Collective Management Organization (CMO) societies. In the US it is called the publishing stream, but in Central Europe it is dominated by author societies, so we modified the label to author’s stream.

Figure 1.1: The Thee Income Streams

The music industry became divided in 1909 when the U.S. Supreme Court denied copyright protection for phonographic rolls. The phonographic industry, which changed from rolls to record plates and later to CDs and digital albums, sought intellectual property protection in the form of neighbouring rights. The exploitation of neighbouring rights creates separate revenue streams for record publishes and self-published musicians. From the 1930s the recording industry far surpassed the music publishing business worldwide and became the dominant revenue source for the whole industry until the 2000s.

In the 2010s, the live performance stream has generated the most revenues in many developed and emerging markets, and it is especially important in Central Europe. The live performance stream has an exceptionally strong input to employment, given that live performances create jobs in transportation, in venues and related accommodation, as well as in the food and beverages industries, where many enterprises cannot serve their clients without live or recorded music. Food and beverage services are themselves the second largest European employer after construction; their tourism-related segment is also a large service exporter. Unlike the other two streams, live performances do not receive but pay musical royalties to the authors. Neighbouring rights are not involved unless the live performances are recorded and published in audio or audiovisual recordings.

1.2 Music Demand

1.2.1 Audience data

We measure audience data with statistically well-designed surveys.

A working group of Eurostat and many national statistical offices within the ESSnet Culture working group has reviewed the best practices in survey design and survey harmonization in 2012. Standardized CAP surveys allow the use of comparison with international surveys, such as the CAP surveys carried out by the European Union and with other countries, which allow the use of standardized evaluation of the survey results.

The Final Report of the Woking Group European Statistical System Network on Culture (in short: ESSnet-Culture) (Bína, Vladimir et al. 2012) contains a rather detailed guideline in the report of the Task Force on Cultural Practices And Social Aspects Of Culture, which contains a very mature social scientific model to measure participation, and survey methodology and samples description on how to carry out such surveys. CEEMID has carried out so far 7 detailed, nationally representative CAP surveys for music and audiovisual use, which it retrospectively harmonized with EU 2007 and EU 2013 surveys (see ?? Annex - Survey harmonization.)

We have analyzed the differences among various regional markets of music in Europe in the Chapter 2 The Audience of Music of the Central European Music Industry Report 2020.

1.2.2 Demand drivers

Cultural economics and our statistical analysis have identified important drivers of demand. These are measurable indicators that increase the likelihood of a person to attend a concert or to buy a record.

These indicators will be reported in downloadable format here.

- Household spending on culture and recreation (in euros and adjusted for purchasing power)

- Education level

- Percentage of population in the 15-24 years cohort

1.2.2.1 Ownership of CD players

The following two indicators are use cases of our eurobarometer software package that allows us to create statistical indicators from the usually unpublished, unused questionnaire data of Eurobarometer.

We can create exclusive, international indicators, or comparisons with Latin America, Africa and the Arab world.

1.2.2.2 Ownership of smartphones

1.2.3 Seasonality

One of the most important aspects of the viability of live music is seasonality. While cultural infrastructure and the income of performers, composers, technicians and managers must be financed throughout the year, concert demand in Europe is extremely seasonal. In emerging markets, as much as 25% of all the demand concentrates (in non-pandemic years) around December. (See: CEE Music Industry Report 2020 - 2.1 Seasonality Concentrated Demand)

There are no centralized data sources for ticket sales in Europe. Therefore, we are sampling various “big data” APIs, such as Google Trends or Foursquare. Our experience shows that where we can cross-check with actual sales, these API data follows actual demand with about 95% precision.

Google Trends does not have a documented API, and only gives out a sample of search intensities, relative to the peak search intensity for up to 5 territories. This means that an EU-wide indicator must be created with several, consistent, standardized and normalized queries. This information is available at both national and regional levels, and for major cities.

Google Trends does not have a documented API, and only gives out a sample of search intensities, relative to the peak search intensity for up to 5 territories. This means that an EU-wide indicator must be created with several, consistent, standardized and normalized queries. This information is available at both national and regional levels, and for major cities.

Foursquare gives far more precise information, but its API does not allow the storage of individual information beyond 30 days. Analytical tools can be built on research data, or statistically aggregated information can be stored about relative visiting intensities for cities, metropolitan areas, regions or countries.

1.3 Private Copying

1.3.1 Use Of Cloud Services

1.3.1.1 Among Students

1.3.1.2 Among Prime Music Age Group

The primary age group of music listening, and also for forming listening habits and tastes is the age group of 16-24.

1.4 COVID-19 Impact

Our COVID-impact indicators are created from Google’s Community Mobility Reports with the help of our regions software package that maps Google’s data to Europe’s regions to make it comparable with Eurostat and other national data.

1.4.0.1 Avarage Change in Retail Visits, Country Level

1.4.0.2 Avarage Change in Retail Visits, Regional Level

1.5 Music Supply

The creation and live and recorded performance of music is different in the case of popular music and classical music, and has special characteristics for jazz and world music.

Throughout the world, the cultural sectors, and music in particular, are dominated by freelancers and micro-enterprises. In European countries, freelancers and micro-enterprises are subject to various simplified tax and financial reporting requirements, and are exempted from most mandatory statistical reporting. Furthermore, they often creatively combine various economic activities, such as performing arts and technical services. As a consequence of this, the creators of music are often invisible for policymakers, because official statistics omit them.

We have been surveying music professionals with an increasing geographical reach since 2014 to fill in those gaps. Our surveys serve two purposes:

- To collect primary data from music creators;

- To establish realistic parameters for estimating the share of music from official, larger statistical groups such as

NACE 59 of the Section J Publishing, audiovisual and broadcasting activitiesfor sound recordings orNACE 90 of the R Arts, entertainment and recreationfor performing arts.

1.5.1 Creators & Creative Professionals

Musicians and their bands create new music works, they record them, and in most cases in Europe they are self-producing and self-publishing their work. Because of the small revenues in these markets, there is little specialization. Creators often must play several artistic, managerial and technical roles, and even this way they cannot make a living from music alone.

For example, technical roles related to the production and distribution of sound recordings belong to division NACE 59 of the Section J Publishing, audiovisual and broadcasting activities of the statistical classification of economic activities in the EU countries, whereas creating music works and performing them belongs to Section NACE 90 R Arts, entertainment and recreation. Creative workers usually build a multi-path career that incorporates various economic activities. Many musicians, including rather popular, successful ones, have other jobs because they cannot make a living relying solely on music-related activities.

Our surveys try to cut through this clutter and make the work of musicians, music technicians and music managers visible.

We will be publishing here 1-2 regularly refreshed indicators in consultation with our partners.

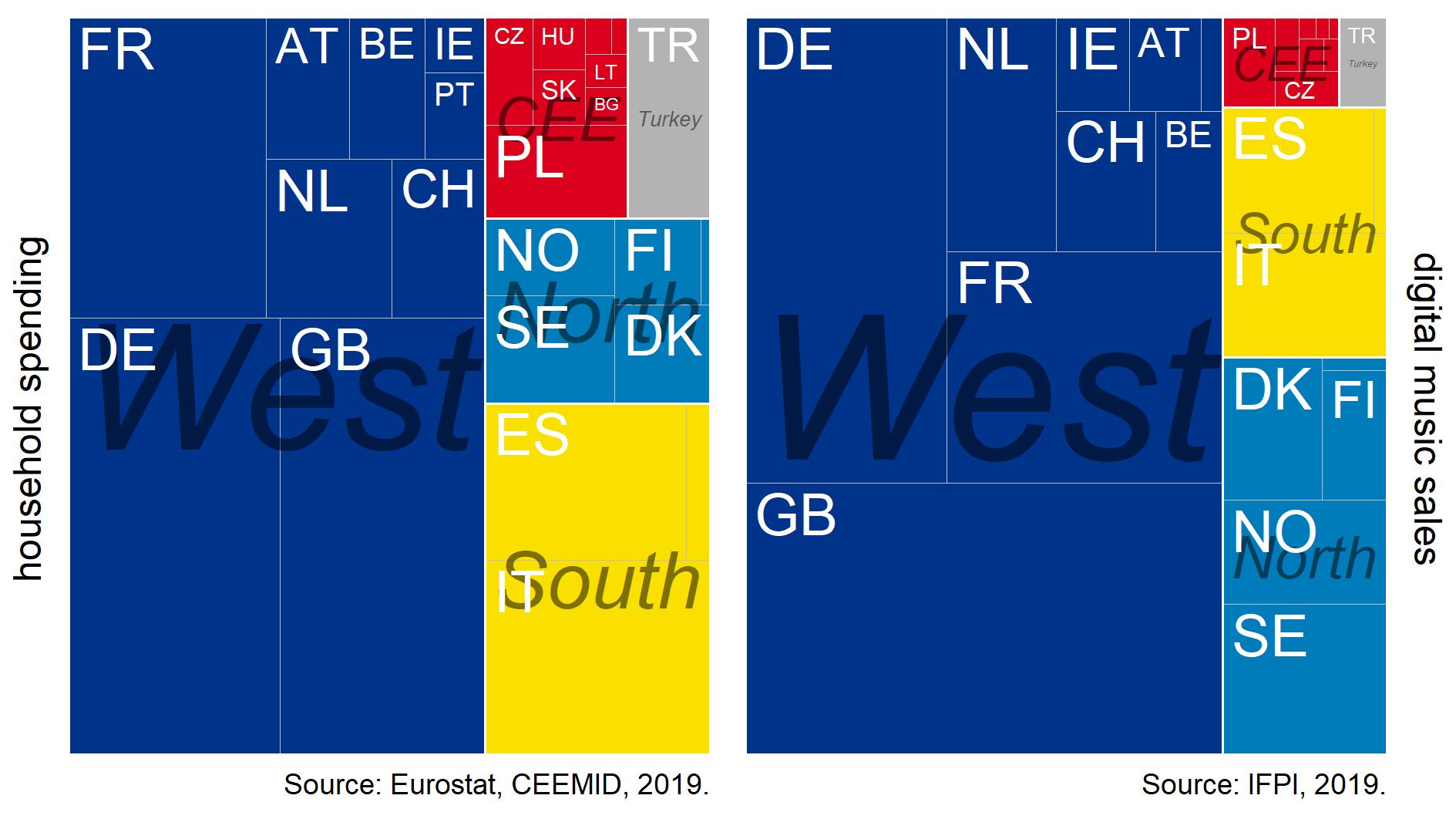

1.5.2 Recorded Market

For our partners in the recording industry, we perform various data analyses, mainly to calculate the value of music and to set royalty tariffs or compensation levels.

For example, we compared the cultural spending of households (not GDP! not salaries! not total spending!) with digital sales in the same European countries in euros.

It is visible in this chart that the potential market in CEE and Southern Europe and Turkey is much bigger than the current one. We are analyzing for our partners the reasons behind this “royalty gap”.

- Part of the difference is attributed to higher levels of piracy and private copying (we have indicators to prove this.)

- Part of the difference is attributed to wrong price levels (sometimes too low and sometimes too high, leading to low sales.)

- Part of the difference is due to weaker music businesses that need to develop their business in order to target a larger part of the household cultural budget.

We are seeking their permission to re-publish these indicators in full for these charts.

1.5.3 Publishing Market

For our partners from the composer and publisher side of the music industry, we are able to perform various data analyses, mainly targeted towards calculating the value of music and setting royalty tariffs or compensation levels.

We are seeking their permission to re-publish 1-2 indicators from these sources here.

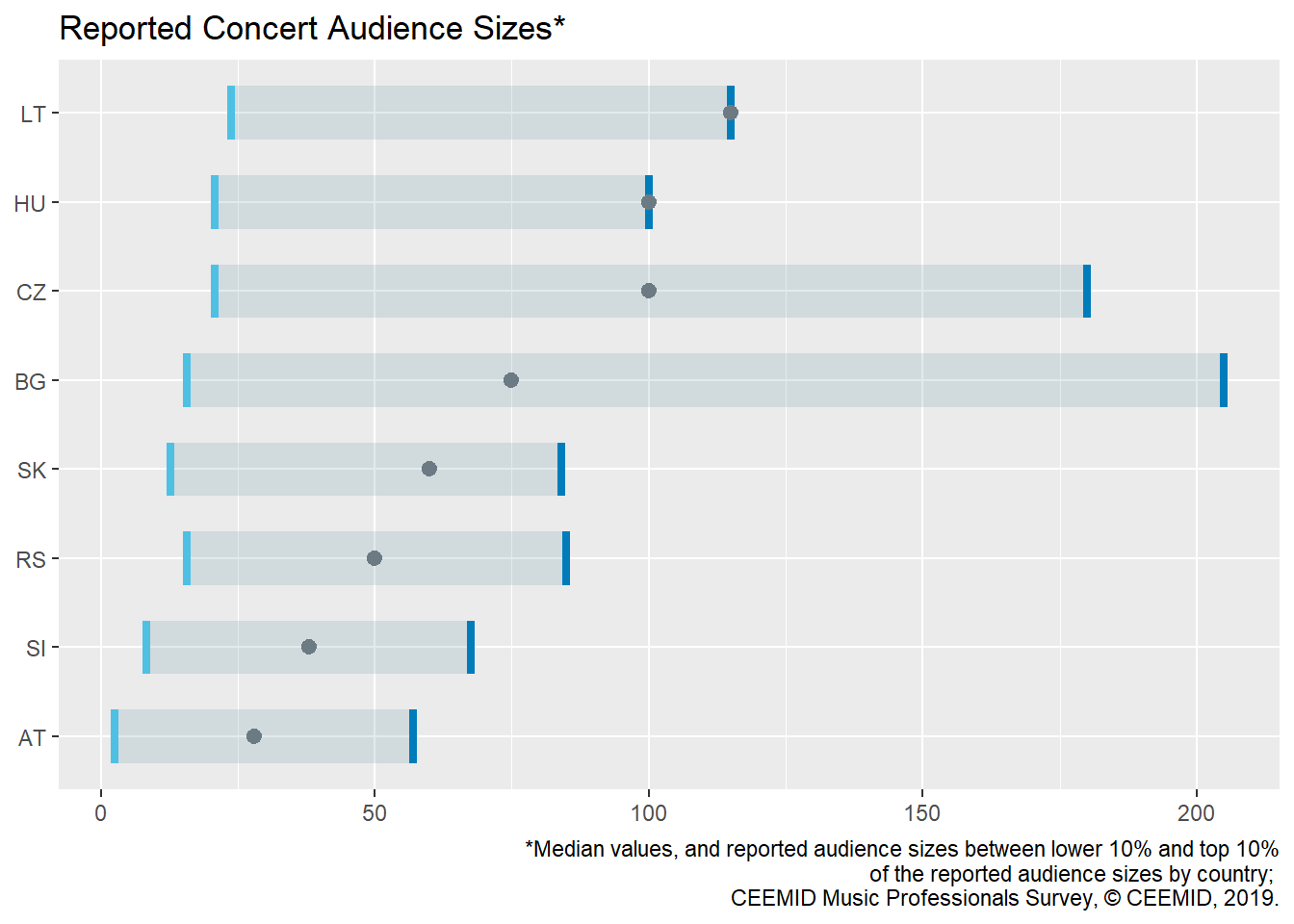

1.5.4 Live Market

We would like to release and regularly maintain a few indicators about live music even though the live music sector is currently largely frozen due to the COVID-19 pandemic.

We are also working on a factual, evidence-based Music Recovery Report that will be made in a similar format to our 2020 music industry report. For some ideas, click over to the Live Music Markets chapter.

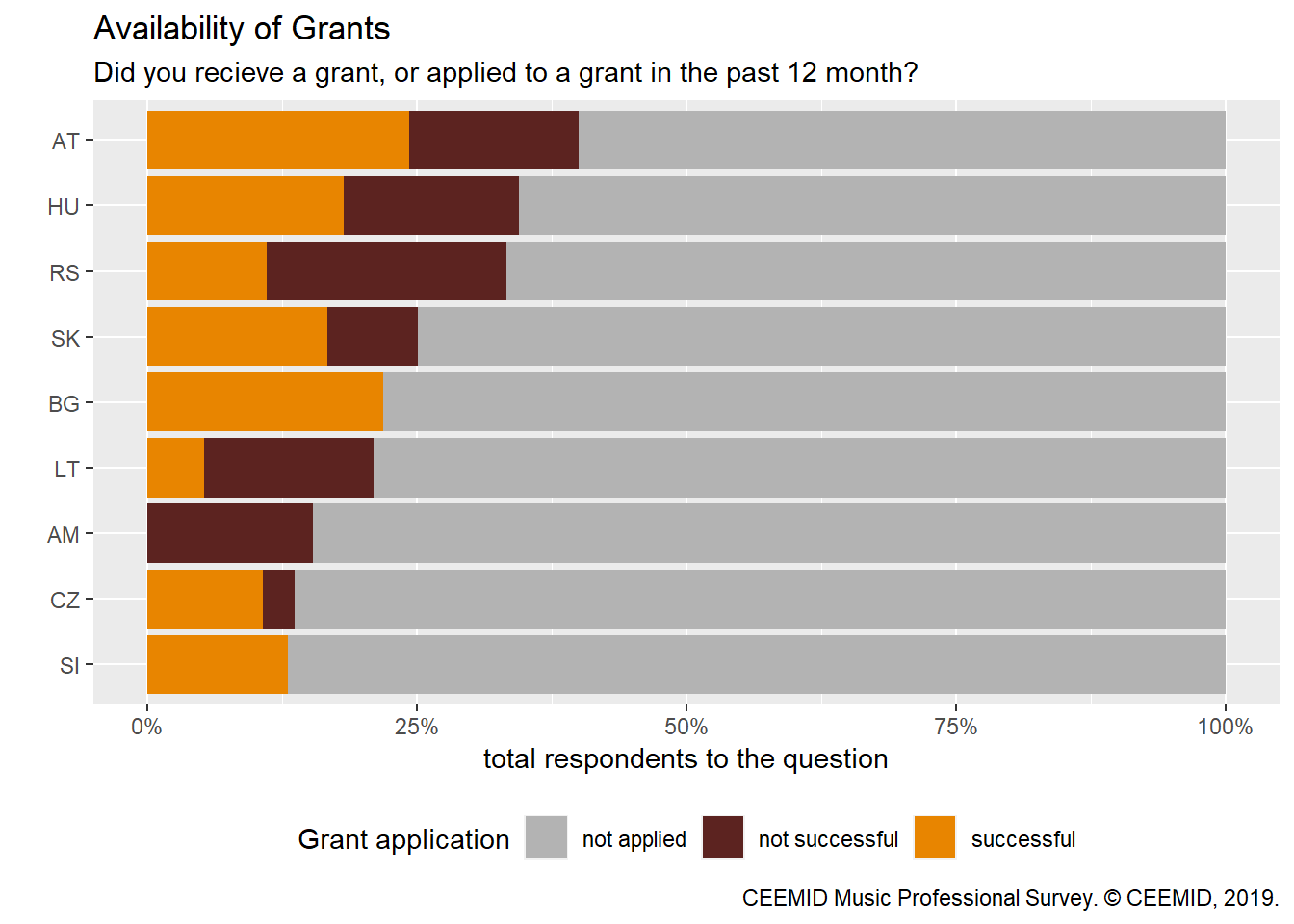

1.6 Grants

Throughout Europe, national, regional and local governments subsidize cultural activities, practices, and cultural enterprises. In our 2019 survey we asked musicians in 12 countries about their grant application success.

Grants are usually not a very large part of the music sector’s income, but they can make a substantial difference if they are adequately targeted.

We are helping granting agencies to set realistic parameters for their grant calls and to evaluate their applicants objectively. We would also like to help with ex post analysis of grants to improve the efficacy of future calls.

References

Bína, Vladimir, Chantepie, Philippe, Deboin, Valérie, Kommel, Kutt, Kotynek, Josef, and Robin, Philippe. 2012. “ESSnet-CULTURE, European Statistical System Network on Culture. Final Report.” Edited by Frank, Guy. http://ec.europa.eu/culture/our-policy-development/documents/ess-net-report-oct2012.pdf.

Hull, Geoffrey P., Thomas W. Hutchison, Richard Strasser, and Geoffrey P. Hull. 2011. The Music Business and Recording Industry Delivering Music in the 21st Century. New York: Routledge. http://search.ebscohost.com/login.aspx?direct=true&scope=site&db=nlebk&db=nlabk&AN=345262.

Leurdijk, Adnra, and Nieuwenhuis Ottilie. 2012. “Statistical, Ecosystems and Competitiveness Analysis of the Media and Content Industries. The Music Industry.” 25277 EN. Edited by Jean Paul Simon. Luxembourg: Publications Office of the European Union, 2012: Joint Research Centre Institute for Prospective Technological Studies (IPTS). http://ftp.jrc.es/EURdoc/JRC69816.pdf.